Voda Market Currents - September 2025

- Danny Lee

- Sep 18, 2025

- 3 min read

Updated: Feb 27

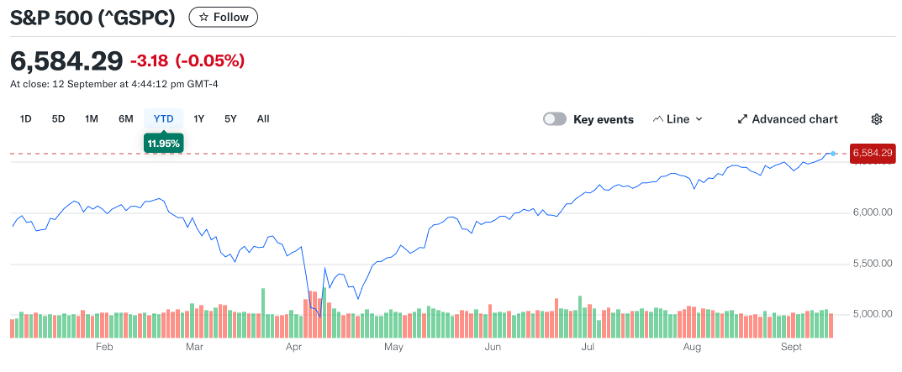

Markets have been resilient in 2025 despite trade uncertainty and shifting policy expectations. The tentative pause in tariffs earlier this year sparked a rebound, with the S&P 500 closing at 6,584.29 on 12 September — about 12% year-to-date, supported by strong corporate earnings and steady consumer demand.

Recent Market Developments

Earnings Strength

· 84% of S&P 500 companies beat forecasts, delivering ~11% YoY earnings growth.

Tech leaders (“Magnificent Seven”) continued EPS growth.

Industrials and autos faced margin pressure from higher input costs.

Takeaway: Earnings breadth supports resilience, but cost pressures remain a drag on cyclicals.

Bond Rally

Powell’s dovish Jackson Hole remarks triggered inflows into bonds.

The US 10-year yield is around 4.06%.

Investors are reallocating into investment-grade credit and REITs ahead of expected cuts.

Takeaway: Fixed income is reclaiming its role as stabiliser and income source.

Currencies in Flux

The US dollar had its weakest first half in 50 years (–10–11%) before a modest July recovery.

Commodity-linked currencies (CAD, BRL, INR) remain pressured by tariffs and slower trade.

Takeaway: USD remains volatile, commodity currencies remain fragile.

Europe

ECB held rates steady at 2% in July.

Minutes reveal a split: some members warn of slowing growth, others focus on inflation risk.

Asia

Japan’s Nikkei 225: +4.7% in August, +10.5% YTD, supported by reforms and AI-related demand.

China: MSCI China +44% YTD, driven largely by retail flows.

India: –3.1% YTD; ASEAN remains positive, supported by supply chain shifts.

Policy and the Fed – All Eyes on September

Latest move: On 17 September, the Federal Reserve cut rates by 25 basis points, the first step in what markets expect to be a series of cuts.

Big banks forecast: Morgan Stanley and Deutsche Bank continue to expect two more Fed rate cuts in 2025 (Oct, Dec).

PIMCO’s view: Powell is more worried about labour market weakness than runaway inflation. Tariff-related inflation is a concern, but a wage-price spiral is unlikely.

The takeaway: The first cut confirms the Fed’s dovish tilt. Expect measured, data-dependent easing — balancing inflation risks with fragile employment trends.

Fund Flow Trends (as of 5 September 2025)

Equities: Strong inflows into US tech and India/ASEAN. Europe lags, with selective strength in defence and infrastructure.

Fixed Income: Bonds in demand. Inflows strong into investment-grade and shorter-duration strategies.

Commodities: Gold (~$3,670–3,700/oz, +38% YoY) continues to draw inflows as a hedge; oil faces persistent outflows.

Regional: China’s rally is still retail-driven, while India and ASEAN continue to see steady institutional support.

Why fund flows matter: Historical performance shows what has worked, and macro data gives us the backdrop. But flow data reveals real-time investor conviction — where capital is actively moving today. Combining all three gives us the clearest picture of where opportunities lie.

Looking Ahead

Cyclical boost from cuts: Rate-sensitive sectors (real estate, utilities, cyclicals) may gain two further cuts are expected.

Megatrends still dominate: AI buildout, energy transition, healthcare & longevity, Asia’s demographic rise, resilient income.

Risks to watch: US labour softness, geopolitical uncertainty, tariff-driven inflation.

Our Guidance

Stay invested — avoid timing Fed meetings.

Diversify across equities, bonds, and alternatives.

Tilt portfolios toward structural themes backed by both earnings and flows.

Why It Matters

Markets are preparing for a shift in policy. But the more important signal is that capital is already moving: into US tech, into Asia, into bonds, and into gold.

This isn’t about chasing headlines. It’s about positioning where conviction is strongest — and where resilience and growth are most likely to come in the years ahead.

Disclaimer:

The information provided in this article is for general informational purposes only and does not constitute financial advice. While every effort has been made to ensure the accuracy of the content, financial decisions should be based on your own research and consultation with a licensed financial adviser.

Comments